azqrujmy

Global Real Estate Trends: Challenges and New Opportunities

Emerging Trends in Global Real Estate

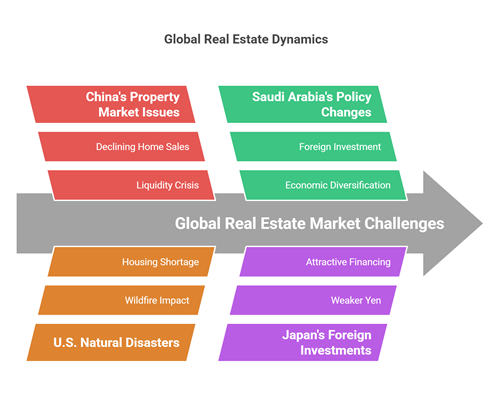

In the ever-evolving world of real estate trends, recent headlines reveal how local and global factors reshape the industry. From challenges in China’s property sector to natural disasters in the U.S. and bold policy changes in Saudi Arabia, these stories offer a comprehensive view of the market’s current state. Let’s look at some of these developments and consider their broader implications.

China’s Property Market: Signs of Stress

The struggles of Vanke, one of China’s largest property developers, serve as a key example of the challenges facing the nation’s real estate market. With a projected $6.2 billion annual loss and the sudden resignation of its chair and CEO, the company’s turmoil reflects deeper systemic issues. The sector, which has been grappling with a liquidity crisis since Evergrande’s collapse in 2021, continues to see declining home sales and mounting debt obligations. While policymakers have introduced measures to stabilize the market—such as encouraging state-owned enterprises to buy unsold housing—the overall investment environment remains shaky. These challenges have dampened homebuyer confidence, raising questions about whether China’s real estate sector can regain its footing shortly.

Los Angeles Wildfires: A Strain on Housing

On the other side of the globe, Los Angeles County faces different real estate pressures due to devastating wildfires. The Eaton and Palisades fires began in early 2024 and have put more than $40 billion worth of residential real estate at risk. Reconstruction costs are staggering, but the long-term effects are equally concerning. Even before the fires, Los Angeles had a well-documented housing shortage, with new household formation outpacing construction. The displacement caused by the wildfires has further tightened the rental market, pushing higher rents in a region already known for its housing affordability issues. This added strain will likely continue, highlighting the need for short-term recovery efforts and long-term strategies to address housing shortages and improve resilience against future natural disasters. New York Post

Saudi Arabia’s Opening of Holy City Real Estate to Foreign Investment

In a groundbreaking move, Saudi Arabia has decided to allow foreign investment in publicly listed companies that own property in Mecca and Medina. This policy, part of the nation’s Vision 2030 economic reform agenda, seeks to attract international capital while maintaining certain restrictions—such as capping foreign ownership at 49%. By opening up the market, Saudi Arabia aims to enhance liquidity and drive growth in the real estate sector, particularly for projects tied to Islamic pilgrimage. This change has already led to increased investor interest, as evidenced by stock gains for key developers in the region. If successful, this initiative could boost the local market and set a precedent for broader economic diversification in the Gulf region.

Brookfield’s Big Moves in Japan

Meanwhile, Canada’s Brookfield Asset Management has taken bold steps in Japan, acquiring a stake in the prestigious Gajoen complex in Tokyo and land for a logistics warehouse near Nagoya. Together, these deals total $1.6 billion and signal a growing trend of foreign investment in Japanese real estate. A weaker yen and attractive financing options have made Japan an appealing destination for international investors. Brookfield’s focus on urban luxury properties and industrial facilities highlights the diverse opportunities available in this market. As more global players enter Japan’s real estate sector, this trend could lead to increased competition and a redefined landscape for Japanese property investments. Reuters

Conclusion: What These Developments Mean

These recent events showcase the challenges and opportunities shaping today’s real estate market. Whether the government’s interventions will stabilize a declining sector in China remains. In the U.S., the wildfires in Los Angeles underscore the need for greater resilience in housing supply. Saudi Arabia’s decision to open its holy city real estate to foreign investors demonstrates the potential for bold policy changes to drive market growth. At the same time, Brookfield’s investments in Japan highlight the appeal of stable, attractive international markets.

Looking ahead, these Real Estate trends will likely influence investor strategies, policymaker decisions, and the overall direction of the global real estate market. Whether through innovative policy changes, increased international investments, or proactive measures to address environmental risks, the real estate sector continues to evolve in response to a complex array of global forces.

Latest Real Estate News: Sales, Wildfires & Luxury Ventures

Navigating the Shifting Landscape of Real Estate

The latest real estate news continues to face a range of transformative challenges and opportunities. From fluctuating sales numbers to environmental impacts and new ventures, the landscape is constantly evolving. This post explores the key trends and recent developments shaping the industry, from declining U.S. home sales to changes in California’s housing market and the emergence of a new player in luxury real estate. Finally, we’ll consider what these shifts mean for the future.

U.S. Home Sales at a Historic Low

In 2024, existing home sales in the United States fell to their lowest level since 1995. This marked the second consecutive year of diminished sales activity, with persistently high mortgage rates being a primary driver. Despite the Federal Reserve cutting short-term interest rates multiple times, mortgage rates remained above 7% for much of the year. Coupled with rising home insurance premiums and property tax expenses, this made homeownership increasingly unaffordable for many Americans.

The result was a cautious market, with both buyers and sellers hesitant to move forward. Inventory levels remained tight, keeping home prices elevated despite lower sales volume. For instance, home prices remained slightly below their mid-2024 record highs yet still climbed steadily due to limited availability. This challenging environment has left the real estate industry wondering: Will mortgage rates come down enough to revive sales in the coming years, or will we continue to see sluggish activity?

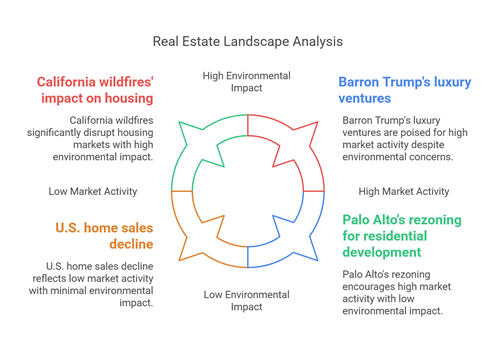

California Wildfires and the Housing Market

In Los Angeles County, the Eaton and Palisades wildfires have underscored the devastating impact of natural disasters on real estate. These fires, which began in early January 2024, threatened more than 15,800 homes valued well above the county’s median price. The total reconstruction costs for affected properties, both residential and commercial, were estimated at over $13 billion.

Beyond the immediate financial toll, the wildfires exacerbated an already strained housing market. Southern California was already grappling with a housing shortage—demand far outpacing supply—and the fires further tightened the market. Many residents were displaced, creating increased pressure on the rental market, which had already been one of the most expensive in the nation. While rental vacancies were at a decade-high late last year, the sudden spike in demand is expected to push rents even higher, adding another layer of complexity to the region’s housing crisis.

A New Luxury Real Estate Player: Barron Trump

Meanwhile, a new luxury real estate company is set to emerge. Barron Trump, the youngest son of Donald Trump, plans to relaunch Trump, Fulcher & Roxburgh Capital Inc., a firm initially incorporated in Wyoming. The company will focus on high-end developments in Utah, Arizona, and Idaho, with headquarters at Mar-a-Lago, Florida. While Barron has received business advice from his father, the venture is not financially backed by the Trump Organization.

Despite the potential for ethical concerns—especially if there are undisclosed investments from Donald Trump—Barron is positioning himself as a serious player in the luxury real estate sector. His team includes classmates from preparatory school, and the company’s projects will likely attract attention from affluent buyers in these rapidly growing states. This new venture could signal a fresh chapter in the Trump family’s real estate legacy if successful. The Times

Rezoning in Palo Alto: A New Housing Frontier

Back in California, Palo Alto has recently taken a bold step by rezoning Stanford Research Park to allow for residential development. Spanning over 700 acres, this traditionally commercial area could soon include new housing options. The rezoning effort is part of a broader push to address the region’s severe housing shortage.

If implemented effectively, this transformation could provide much-needed relief to the housing crunch, adding inventory in one of the most competitive markets in the state. However, it will also require careful planning to balance the needs of businesses, residents, and the surrounding community. With such a large-scale change, local authorities will need to ensure that infrastructure, transportation, and community services can keep pace with the anticipated growth.

What Lies Ahead?

The current real estate landscape presents a mix of challenges and opportunities. On one hand, rising costs, high mortgage rates, and environmental impacts are straining affordability and availability. Conversely, new ventures and rezoning initiatives point toward innovative solutions and growth potential. Whether the market can overcome these hurdles will depend on several factors: the direction of mortgage rates, the industry’s ability to adapt to environmental risks, and the effectiveness of new development projects.

As we move into the next phase of this ever-changing market, one thing is clear: adaptability and creative problem-solving will be key. By keeping a close eye on these trends and anticipating future shifts, industry professionals and homebuyers alike can better navigate the complexities of the real estate sector.

Latest Real Estate Trends: Luxury, REITs & Government Sales

Recent Real Estate Trends and Developments in the Real Estate Market

In recent months, the real estate sector has seen a flurry of activity and notable shifts. The market continues evolving, from government property sales to luxury home transactions, creating opportunities and challenges. Here’s a closer look at the latest trends and headlines:

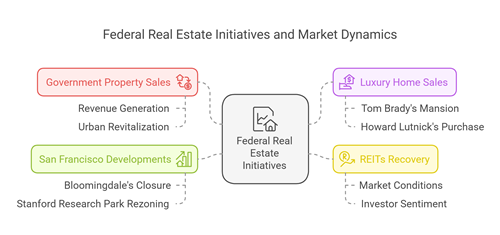

Federal Government Real Estate Downsizing

Efforts to reduce the federal government’s real estate footprint have gained momentum. Initially sparked during the Obama administration, these initiatives have ramped up under the Trump administration. In fiscal year 2024, the General Services Administration (GSA) reported a remarkable $710 million in revenue from government property sales. These transactions bring revenue and offer private investors the chance to repurpose older office spaces, potentially revitalizing urban communities and breathing new life into local economies. Marketwatch

High-Stakes Luxury Home Sales

The luxury real estate market is also making waves. One of the most talked-about upcoming sales involves Tom Brady’s newly completed waterfront mansion on Indian Creek Island in Florida. Expected to list at over $150 million, this property has the potential to set a new record for home sales in Miami. In Washington, D.C., the luxury market is equally vibrant. High-profile deals, such as Howard Lutnick’s purchase of Bret Baier’s home in the prestigious Foxhall area for $25 million, underscore the growing demand for top-tier properties in the capital. WSJ

A Glimmer of Hope for REITs

After facing a challenging year, Real Estate Investment Trusts (REITs) are showing signs of recovery. The Real Estate Select Sector SPDR ETF (XLRE) experienced underperformance throughout 2024, but it still holds notable names like Prologis, American Tower, Digital Realty, and Equinix. As Treasury yields stabilize and investors closely monitor inflation concerns, the stage may be set for a REIT rally. However, caution remains the watchword as market conditions continue to shift.

San Francisco’s Shifting Real Estate Landscape

San Francisco and Palo Alto are seeing significant real estate developments in the Bay Area. San Francisco’s Bloomingdale’s flagship store is preparing to close its doors at the San Francisco Centre mall, marking a significant change for the half-empty shopping center near Union Square. Meanwhile, Palo Alto’s decision to rezone Stanford Research Park to allow housing could transform the 700-acre business campus into a mixed-use area, potentially creating new residential opportunities and reshaping the local market. Real deal

Conclusion

From government downsizing to high-profile luxury deals and the evolving roles of REITs, the real estate landscape is as dynamic as ever. Whether you’re an investor, homeowner, or market observer, staying informed on these shifts can help you navigate this ever-changing sector.

Mortgage Rates Unveiled: What This Means for Homebuyers

Mortgage rates have been a hot topic lately, and as of January 19, 2025, they continue to display slight fluctuations, though the overall market remains stable. If you’re looking to buy a home or refinance your existing mortgage, understanding these trends can help you make more informed decisions.

Today’s 30-Year Fixed Rate Snapshot

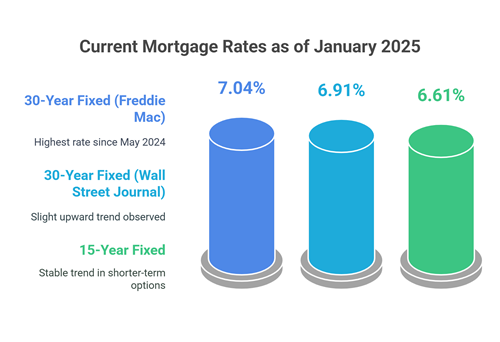

According to Mortgage News Daily, the average 30-year fixed mortgage rate is currently 7.07%. This figure represents a modest dip from earlier in the week, indicating some relief for borrowers after a period of slow upward creep. Forbes Advisor also cites a similar number, pegging the average rate at 7.04%. While minor differences exist depending on the source, the overall picture suggests that rates are holding steady.

Current Mortgage Rates

- 30-Year Fixed Rate:

-

- Freddie Mac reports an average rate of 7.04% for the week ending January 16, 2025, marking the fifth consecutive week of increases, and the first time rates have surpassed 7% since May 2024.

- The Wall Street Journal notes an average rate of 6.91% as of January 6, 2025, indicating a slight upward trend.

-

- 15-Year Fixed Rate:

-

-

- The average rate is 6.61% as of January 13, 2025, reflecting a stable trend in shorter-term mortgage options.

-

Recent Trends and Fluctuations

Over the past few weeks, economic factors have influenced mortgage rates, including inflation data and Federal Reserve policy signals. In early January, rates began to rise due to signs of persistent inflation and hints that the Fed might be cautious. Despite these pressures, rates have not surged dramatically, giving borrowers time to assess their options.

Market Stability and Context

While the 30-year fixed rate remains above 7%, stability in the market suggests that we’re not facing a sudden spike. Instead, borrowers can approach their mortgage plans with a sense of measured urgency—acting before rates climb further, but without fearing an immediate dramatic increase. This relatively calm environment may encourage more buyers to enter the market, particularly those waiting for rates to plateau.

Market Influences

Economists have adjusted their inflation forecasts upward due to proposed policies from President-elect Donald Trump, including raising tariffs, cutting taxes, and restricting immigration. The consumer-price index is expected to increase by 2.7% in December 2025, up from an earlier projection of 2.3%. This anticipated rise in inflation could exert upward pressure on both inflation and interest rates, potentially affecting mortgage rates in the coming months.

What This Means for Homebuyers and Refinancers

For prospective homebuyers, today’s rates offer a more apparent baseline for planning monthly budgets. Knowing that the market isn’t experiencing wild swings allows for more predictable decision-making. Those looking to refinance can also benefit by comparing current rates to what they’re paying now, potentially locking in savings before any future rate increases.

Housing Market Trends

The housing market has seen a strong start in 2025, with a record number of new properties listed, providing buyers with increased options. Rightmove reported an 11% increase in new listings compared to last year’s period, along with a record number of mortgage-in-principle applications. This surge has led to the highest level of buyer choice since 2015. Additionally, the average property price has risen by 1.7% this month, the most substantial increase since 2020, although prices remain below last year’s peak due to affordability constraints.

Looking Ahead

While mortgage rates have experienced slight increases, they remain relatively stable. However, potential policy changes and economic factors could influence future trends. Prospective homebuyers and those considering refinancing should stay informed about these developments to make well-informed decisions.

Final Thoughts

As of January 19, 2025, mortgage rates show subtle movement within a generally stable market. Keeping an eye on sources like Mortgage News Daily and Forbes Advisor can help you stay informed. By understanding these trends and consulting with mortgage professionals, you can make better financial decisions whether purchasing a new home or exploring refinancing options.

U.S. Housing Market Outlook for 2025:

Trends, Predictions, and Opportunities

The U.S. housing market has always been a cornerstone of the country’s economy, influencing everything from job creation to wealth building. As we look ahead to 2025, understanding the market’s trajectory is essential for homebuyers, investors, and policymakers. In this article, we explore key trends, predictions, and opportunities in the housing market for 2025.

Current Trends Shaping the Housing Market

Shifts in Homebuyer Demographics

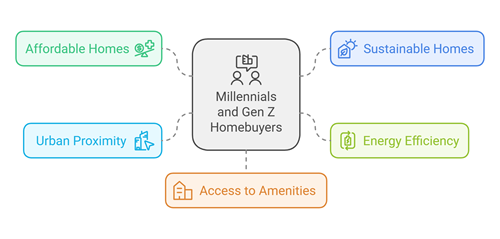

Millennials and Gen Z are entering the housing market more significantly, driving demand for affordable and sustainable homes. These younger buyers prioritize energy efficiency, proximity to urban centers, and access to amenities.

Rising Mortgage Rates

As the Federal Reserve continues to adjust interest rates to manage inflation, mortgage rates are expected to remain higher than the historic lows of recent years.

For first-time buyers, this could mean a more challenging time qualifying for loans or affording monthly payments, prompting many to consider smaller homes or alternative financing options.

Retirees may find it challenging to downsize or relocate due to higher borrowing costs, potentially opting to stay in their current homes longer. These dynamics will likely shift demand toward more affordable housing and innovative mortgage solutions.

As the Federal Reserve continues to adjust interest rates to manage inflation, mortgage rates are expected to remain higher than the historic lows of recent years. It will affect affordability and shift demand toward smaller homes or alternative financing options.

Remote Work’s Lasting Impact

The pandemic revolutionized our work, and remote or hybrid models are here to stay. Suburban and rural areas with robust digital infrastructure are seeing increased interest as buyers seek larger homes at lower costs.

Predictions for 2025

Moderation in Home Prices

After years of skyrocketing prices, the market is expected to cool slightly, with home prices stabilizing in most regions. Areas such as the Midwest and parts of the Southeast are likely to see more significant moderation due to balanced supply and demand dynamics. Meanwhile, high-demand regions like the West Coast may experience slower growth rather than outright declines, reflecting ongoing urban desirability. After years of skyrocketing prices, the market is expected to cool slightly, with home prices stabilizing in most regions. While some areas may still experience growth due to local demand, affordability concerns will likely cap dramatic increases.

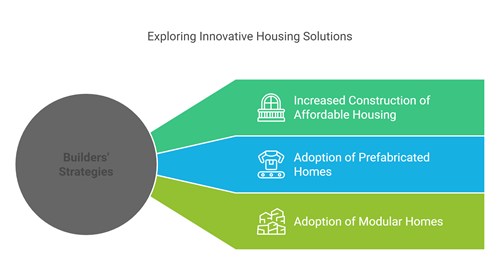

Increased Supply Through New Construction

Builders are ramping up efforts to meet demand, particularly in the affordable housing sector. Prefabricated and modular homes are gaining traction as cost-effective solutions.

Greater Emphasis on Sustainability

Eco-friendly building materials and energy-efficient designs will become the norm as both builders and buyers recognize the long-term value of sustainability.

Opportunities for Homebuyers and Investors

For Homebuyers:

- Explore First-Time Buyer Programs: Many state and federal programs offer down payment assistance and lower interest rates for eligible buyers.

- Consider New Construction: With increased supply, new homes may offer better value, modern features, and fewer maintenance concerns.

For Investors:

- Look at Growing Suburbs: Suburbs near major cities like Austin, Texas; Raleigh, North Carolina; and Nashville, Tennessee, are poised for growth. These areas attract remote workers seeking affordability, strong job markets, and a high quality of life. Suburbs near significant cities are poised for growth as they attract remote workers seeking affordability and space.

- Focus on Rental Properties: With affordability challenges, demand for rental housing is expected to remain strong.

How to Prepare for the 2025 Housing Market

- Assess Your Finances: Ensure you have a strong credit score (typically 620 or higher for most conventional loans) and aim for a debt-to-income (DTI) ratio below 36%. Additionally, save at least 20% for a down payment to avoid private mortgage insurance (PMI) or consider programs that allow lower down payments if eligible.

- Stay Informed: Follow market trends and consult with real estate professionals to make data-driven decisions.

- Leverage Technology: Use online tools to compare home prices, mortgage rates, and neighborhoods to find the best deals.

Recommended Resources and Services

- Home Buying Tools: Use mortgage calculators and budget planners to understand affordability.

- Real Estate Platforms: Websites like Zillow and Redfin can help you explore listings and market trends.

- Energy Efficiency Experts: Consult professionals to assess or upgrade homes for sustainability.

Conclusion

The U.S. housing market in 2025 is shaping up to be dynamic and filled with both challenges and opportunities. Whether you’re a first-time buyer, a seasoned investor, or simply curious about market trends, staying informed is key to making the most of what’s to come.

Loan for Commercial Property Calculator

Calculate Your Commercial Property Loan Now

Navigating the landscape of commercial real estate investment requires a keen understanding of various financial parameters. One such crucial component is a loan for commercial property, a financial tool that investors or business owners use to acquire or develop commercial properties.

But how do you gauge the affordability of such a loan, keeping in mind the various terms and conditions attached to it? It is where a ‘loan for commercial property calculator’ comes into play.

Commercial Loan Calculator

A loan for commercial property calculator is a sophisticated online tool designed to help potential borrowers determine the financial implications of a commercial loan. By inputting essential loan parameters such as the loan amount, Interest, and loan term, you can estimate your potential monthly payments, total Interest paid, and overall repayment schedule.

This digital calculator aids investors in making informed decisions by providing a clear snapshot of a commercial property loan’s potential costs and profits. It enables you to understand the financial commitment you’re about to make, assisting in creating a solid repayment plan and ensuring that your investment is sound and profitable.

Using a loan for a commercial property calculator doesn’t end with a single calculation. It allows you to modify the variables, providing different scenarios, each giving insights into how changes in the loan amount, interest rates, or loan term can impact your repayments. This invaluable tool can act as your guide to making the best possible choices when it comes to commercial property investment.

The Role of Commercial Loans in Real Estate

Commercial loans play a significant role in facilitating the expansion and development of businesses. As an investor or business owner, these loans offer a powerful means to acquire, develop, or refinance commercial properties. They allow companies to generate cash flow, provide a venue for operations, or gain an appreciating asset. These loans are often the stepping stone for businesses to realize their full potential.

The Power of Calculators in Loan Planning

In the complex world of commercial loans, calculators act as valuable tools for planning and decision-making. They help you understand your potential monthly payments, the total amount payable over the loan term, and how much you can afford to borrow. By providing a clear picture of these vital metrics, calculators simplify the task of budgeting and forecasting, making it easier to plan for your future investments.

Unveiling the ‘Loan for Commercial Property Calculator’

A ‘loan for commercial property calculator’ is an advanced tool designed to help you navigate the terrain of commercial real estate financing. It considers various factors unique to commercial loans, such as the interest rate, loan term, and loan-to-value ratio, to accurately estimate your loan repayment schedule. With this, you can make informed decisions about your commercial real estate investments and ensure they align with your financial goals.

Why This Guide is a Must-Read

Navigating the world of commercial property loans can be daunting, especially if you’re new to the industry. This guide aims to break down these complexities, taking you step by step through the process of understanding commercial loans, the use of a commercial property loan calculator, and how to interpret the results effectively. Whether you’re experienced or just starting, this guide will help you with the knowledge to make smarter, more informed decisions about your commercial property investments.

Understanding Commercial Loans

What are Commercial Loans?

Commercial loans, at their core, are a type of financing specifically designed for business purposes, including purchasing, renovating, or developing commercial properties. These properties include office buildings, retail stores, industrial facilities, and rental properties. Commercial loans are typically offered by banks, credit unions, and other financial institutions and are meant to help businesses grow, expand their operations, or increase their working capital.

Unlike personal loans, commercial loans often have stricter eligibility requirements and involve more significant amounts. The terms of commercial loans, such as interest rates, repayment terms, and collateral conditions, are usually determined by the lending institution’s risk assessment of the borrower’s ability to repay the loan.

Different Types of Commercial Loans

Commercial loans come in various forms, each designed to meet different business needs. Here are some common types:

- Commercial Real Estate Loans: These are used for purchasing or renovating commercial properties. They often have longer repayment terms and lower interest rates, given the collateral’s high value (the property itself).

- Term Loans: These are traditional loans that provide a lump sum of money upfront, which is then paid back over a specific period, usually with Interest.

- Business Lines of Credit: These provide a revolving credit limit that can be used again. They help manage cash flow and unexpected expenses.

- SBA Loans: Offer favorable terms for small businesses.

- Equipment Loans: These are used to finance the purchase of machinery, vehicles, or other equipment for business use. The equipment itself typically secures the loan.

The Real-Life Application of Commercial Loans

Commercial loans have numerous real-life applications, from start-ups looking for initial capital to established businesses seeking to expand. A restaurant owner, for instance, might use a commercial loan to purchase a new location or a term loan to renovate the dining area. A manufacturing company might leverage an equipment loan to update its production machinery. At the same time, a retail store could use a line of credit to stock up on inventory for the holiday season.

One crucial aspect of commercial loans is that they allow businesses to make significant investments or cover expenses without sacrificing operational funds. They allow growth and improvement, even when significant upfront costs are involved. By understanding the different types of commercial loans available and their practical applications, businesses can leverage the right financial tools to meet their objectives and optimize growth.

Diving into Commercial Property Basics

Defining Commercial Property

Commercial properties, sometimes called commercial real estate, encompass all real property used for business activities. Unlike residential properties designed for living purposes, commercial properties serve as a venue for businesses to operate, generate revenue, and grow.

Commercial properties can take various forms, from small retail shops to expansive office complexes or industrial warehouses. The specific function of a commercial property largely depends on its location, design, and the type of business it serves. For instance, a property in a bustling city center might be suitable for retail shops or restaurants. In contrast, a large plot on the city outskirts might be used for industrial activities or warehousing.

The Advantages of Commercial Property Investment

Investing in commercial property offers several advantages, making it an attractive proposition for individual and institutional investors. Here are a few key benefits:

- Income Potential: Commercial properties often yield higher returns on investment than residential properties, mainly due to higher rental rates.

- Long-term Leases: Commercial leases are typically longer than residential ones, providing a more stable and predictable income stream.

- Appreciation: Commercial properties can increase in value over time, leading to capital gains.

- Diversification: Investing in commercial properties allows investors to diversify their portfolios, reducing risk and potential losses from other investments.

The Various Types of Commercial Properties

There are several types of commercial properties, each serving different business purposes:

- Office Buildings: Range from small single-tenant offices to towering skyscrapers in city centers. Businesses typically use them as their headquarters or regional offices.

- Retail/Restaurant: These include shopping centers, malls, standalone retail stores, and restaurant spaces.

- Industrial: These properties include warehouses, factories, and distribution centers for manufacturing, storage, and distribution.

- Multifamily: These are residential properties rented out to tenants, such as apartments and condominiums. While primarily residential, they are considered commercial if they have five or more units.

- Mixed-Use: These properties combine different uses, like a building with retail shops.

- Hotels: These commercial properties provide accommodation services, including small motels and large hotel chains.

- Particular Purpose: These are properties designed for a specific business purpose, such as gas stations, schools, or hospitals.

Understanding commercial properties’ basics and benefits can guide potential investors in making informed decisions that align with their financial goals and risk tolerance.

The Need for a Loan for Commercial Property Calculator

The Significance of Loan Calculators in Commercial Property Investment

A loan for a commercial property calculator plays a pivotal role in commercial real estate investment. It gives investors a bird’s eye view of the financial implications of their proposed venture. By inputting the necessary parameters, such as a loan amount, interest rate, and loan term, the calculator can offer crucial insights into the prospective monthly repayments, total Interest payable, and overall repayment timeline.

It can guide potential borrowers to estimate their possible loan commitment and assess how it aligns with their investment strategy and financial capability. It offers a ‘trial run’ of your proposed loan, helping you gauge whether it is feasible and affordable before approaching the lender.

Leveraging Loan Calculators for Better Financial Planning

A loan for commercial property calculator is more than just a number cruncher; it is a strategic tool for better financial planning. It empowers investors to adjust and experiment with different loan variables, such as varying interest rates or loan terms, providing different outcomes for each scenario. It can prove invaluable in illustrating the long-term financial impact of the loan, aiding in strategic planning and decision-making.

Moreover, by understanding the potential monthly repayments and total loan cost, investors can better budget for the loan, incorporate it into their financial plan, and ensure they remain financially stable throughout the loan period.

Advantages of Pre-calculating Commercial Loans

There are several advantages to pre-calculating a commercial loan using a loan calculator:

- Understanding Affordability: A calculator can help you understand whether you can afford the monthly repayments and the total cost of the loan, helping you avoid overborrowing.

- Comparing Loan Offers: Using a calculator, you can compare different loan offers, interest rates, and loan terms, allowing you to choose the most cost-effective option.

- Planning Repayment: Knowing the monthly repayment amount can help you plan your finances better, ensuring you can comfortably meet the repayment schedule.

- Saving Time and Energy: Using a loan calculator can save considerable time and effort by providing quick and accurate calculations, making the loan application process smoother and more efficient.

In conclusion, a loan for commercial property calculator is an essential tool in the arsenal of any retail property investor. Its ability to forecast financial commitments and illustrate various loan scenarios can provide invaluable assistance in making well-informed and financially sound investment decisions.

How Does a Loan for Commercial Property Calculator Work?

Walking Through a Loan for Commercial Property Calculator

A loan for commercial property calculator works by using the essential loan parameters you provide to compute your potential monthly repayments, total Interest payable, and overall repayment schedule. Here’s a step-by-step walk-through of how you’d typically use one:

- Input the Loan Amount: This is the total amount you intend to borrow to finance the commercial property.

- Enter the Interest Rate: This is the loan’s annual interest rate. This rate can vary significantly based on the lender, your creditworthiness, and market conditions.

- Specify the Loan Term: This is the length of time over which you plan to repay the loan, typically expressed in years.

- Click Calculate: After inputting all the necessary information, click the “Calculate” button.

The calculator then uses this data to estimate your monthly repayments, the total amount payable over the loan term, and a breakdown of how much each compensation goes toward the principal and Interest.

Understanding the Input Variables

In using a loan for commercial property calculator, it’s essential to understand the input variables:

- Loan Amount: This is the principal amount you plan to borrow. The more significant the loan amount, the higher your repayments will be.

- Interest Rate: This is expressed as a percentage of the loan amount. It’s typically applied annually but divided by 12 for monthly repayments—a higher interest rate results in a higher total loan cost.

- Loan Term: This is the duration over which the loan will be repaid. Longer loan terms result in lower monthly repayments but higher total Interest paid over the life of the loan.

Interpreting the Output of the Calculator

After inputting the variables, the loan for commercial property calculator provides the following output:

- Monthly Repayment: This is the amount you’ll be required to pay each month over the loan term.

- Total Repayable: This is the total amount that will be paid back to the lender over the loan term, including both the principal and the Interest.

- Total Interest Paid: This is the total amount of Interest you’ll pay over the life of the loan. It is the difference between the total repayable and the initial loan amount.

- Amortization Schedule: This table shows the breakdown of each payment into principal and Interest and how the loan balance decreases over time.

By understanding the function and interpretation of a commercial property loan calculator, you can better grip your loan planning, aligning it with your broader financial strategy.

Maximizing Benefits of Conventional Commercial Loans for Businesses

Understanding the Advantages of Conventional Commercial Loans

In the business financing landscape, conventional commercial loans stand out as a cornerstone for companies seeking to bolster their operations, finance expansion, or navigate the complexities of financial management. These loans, offered by banks and financial institutions, are not backed by a government entity, distinguishing them from other types such as SBA loans. Despite the myriad financing options available today, conventional commercial loans are popular for businesses due to their distinct benefits. This article explores the intent behind opting for traditional commercial loans and sheds light on their advantages.

Flexibility and Versatility

One of the primary advantages of conventional commercial loans is their flexibility. These loans can be tailored to meet a business’s specific needs, offering varied repayment terms, loan amounts, and interest rates. Whether a company seeks to purchase real estate, invest in new equipment, or boost working capital, conventional loans can be structured to suit these diverse requirements.

Competitive Interest Rates

Conventional commercial loans often feature competitive interest rates, particularly for borrowers with strong credit histories and solid business plans. Lower interest rates translate into lower total borrowing costs over the life of the loan, making this option financially attractive for well-qualified applicants.

Simplified Ownership Structure

Unlike equity financing, where businesses might have to give up a portion of ownership to investors, conventional commercial loans do not dilute the owner’s equity stake. Business owners retain complete control over their operations and decision-making processes, a critical consideration for many entrepreneurs.

Long-term Financial Planning

Conventional commercial loans offer the benefit of fixed repayment schedules, which can be crucial for long-term financial planning and budgeting. Knowing the amount due each month allows businesses to plan their finances more effectively, providing a sense of security and predictability in managing operational expenses.

Building Credit and Relationships

Successfully securing and repaying a conventional commercial loan can significantly enhance a business’s credit profile; furthermore, it establishes a relationship with the lending institution, which could be beneficial for securing additional products or services.

Considerations and Conclusion

While conventional commercial loans offer numerous advantages, businesses should consider their eligibility criteria, which can be stringent. A strong credit history, a solid business plan, and sufficient collateral are often prerequisites.

In conclusion, conventional commercial loans offer flexibility, competitive rates, and financial control, appealing to businesses looking to finance their growth or operational needs. By understanding these benefits, companies can make informed decisions that align with their financial strategies and long-term objectives. It’s advisable to consult with a financial advisor or banker to explore the best financing options tailored to your business’s unique situation.

Navigating the Eligibility Criteria for Conventional Commercial Loans: A Closer Look at the Benefits

When securing financing for your business, understanding the eligibility criteria for conventional commercial loans is crucial. These criteria ensure that banks and financial institutions mitigate their risk and offer significant advantages to borrowers who meet these standards. This simple guide delves into the specific requirements set by lenders for conventional loans, including credit scores, business history, cash flow analysis, and collateral requirements, highlighting how meeting these criteria can benefit your business.

Credit Scores: The Foundation of Trust

A strong credit score is paramount in the world of conventional commercial loans. It is a testament to your business’s financial responsibility and capacity to repay the loan. Achieving and maintaining a high credit score opens the door to lower interest rates, which can significantly reduce borrowing costs over time. For businesses, this means more resources can be allocated toward growth initiatives rather than servicing debt.

Business History: A Record of Success

Lenders typically require a solid track record of operational success, usually at least two years in business. This history demonstrates stability and profitability, assuring lenders that your business is a viable candidate for a loan. Meeting this criterion can also afford businesses more favorable loan terms and amounts, reflecting the lender’s confidence in your business’s longevity and continued success.

Cash Flow Analysis: Demonstrating Repayment Capacity

One of the most critical aspects lenders examine is your business’s cash flow. They want your operations to generate sufficient cash to cover existing expenses plus the new loan payments. A positive cash flow analysis reassures lenders of your ability to manage financial obligations, potentially leading to more attractive loan options. It also underscores the importance of sound financial management within your business, encouraging practices that sustain and enhance your cash flow position.

Collateral Requirements: Securing Your Commitment

Collateral often plays a crucial role in securing conventional commercial loans. It assures lenders that they can recover their funds if a borrower defaults. For businesses, offering collateral can facilitate access to more significant loan amounts and better terms. It also signifies your confidence in your business’s future success and commitment to repaying the loan.

The Benefits of Meeting Eligibility Criteria

Understanding and meeting the eligibility criteria for conventional commercial loans can significantly impact your business’s financial health and growth trajectory. It enhances your ability to secure financing under favorable terms and positions your business as a credible and trustworthy entity in the eyes of financial institutions. Moreover, meeting these criteria encourages sound business practices, such as maintaining a good credit score, ensuring steady business growth, managing cash flow effectively, and appreciating the value of assets.

While the eligibility criteria for conventional commercial loans may seem daunting, they offer a framework for businesses to demonstrate their creditworthiness and operational viability. By meeting these criteria, companies can secure the financing they need and benefit from lower costs, better terms, and a more robust financial foundation. As you navigate the path to securing a conventional commercial loan, remember that these criteria are not just hurdles but opportunities to strengthen and showcase your business’s potential.

Choosing the Right Financing: A Comparative Analysis of Conventional Commercial Loans and Alternatives

Selecting the right financing option is critical for businesses seeking growth or sustainability. Conventional commercial loans are popular, but how do they compare to other financing avenues like SBA loans, lines of credit, merchant cash advances, and venture capital? This article provides a comparative analysis, outlining the pros and cons of each to assist businesses in making informed decisions that align with their unique needs.

Conventional Commercial Loans

Pros:

- Competitive Interest Rates: For businesses with solid credit, conventional loans often offer lower interest rates than alternative financing options.

- Flexibility in Use: Funds can be used for various purposes, including expansion, inventory, or capital expenditures, without specific restrictions.

- Fixed Payment Schedule: Offers predictability in budgeting and financial planning.

Cons:

- Stringent Eligibility Criteria: Requires solid credit scores, substantial business history, and often collateral, which may only be feasible for some businesses.

- Longer Approval Times: The application and approval process can be lengthy, delaying access to funds.

SBA Loans

Pros:

- Lower Down Payments: Generally require smaller down payments than conventional loans.

- Government-backed: Reduced risk for lenders means these loans are often accessible to businesses that might not qualify for conventional loans.

- Favorable Terms: Longer repayment terms and caps on interest rates.

Cons:

- Complex Application Process: The paperwork and requirements can be more cumbersome than conventional loans.

- Use Restrictions: Some SBA loans restrict how the funds can be used.

Lines of Credit

Pros:

- Flexibility: Businesses can draw funds as needed up to a specific limit, making it ideal for managing cash flow and unexpected expenses.

- Interest Only on Amount Drawn: You pay interest only on the amount you use, not the total credit line available.

Cons:

- Variable Interest Rates: Rates can fluctuate, making monthly payments unpredictable.

- Potential for Mismanagement: The ease of accessing funds can lead to overreliance and financial strain.

Merchant Cash Advances (MCA)

Pros:

- Quick Access to Funds: MCAs can provide funds within a few days.

- No Fixed Monthly Payments: Repayments are a percentage of daily sales, which can ease financial pressure during slow periods.

Cons:

- High Costs: Often have higher fees and interest rates than other financing options.

- Short-term Solution: Best suited for immediate, short-term needs rather than long-term financing.

Venture Capital

Pros:

- Considerable Funding Potential: This can provide substantial funds to fuel growth and expansion.

- Non-debt Financing: No need to repay the funds, avoiding debt accumulation.

Cons:

- Equity Dilution: Involves giving up a portion of ownership and control of the business.

- Intensive Scrutiny and Conditions: Investors may require a significant say in business operations and strategic decisions.

Each financing option presents a unique set of advantages and drawbacks. Conventional commercial loans offer stability and competitive rates for qualified businesses, making them an attractive choice for those who meet the stringent criteria. SBA loans provide a government-backed alternative with favorable terms, particularly for those facing hurdles with conventional loan eligibility. Lines of credit and merchant cash advances offer flexible, albeit potentially costly, solutions for immediate cash flow needs. While providing substantial funding, venture capital comes with the trade-off of equity and possible operational oversight.

The best financing option depends on your business’s specific situation, including financial health, immediate and long-term needs, and growth objectives. Evaluating the pros and cons of each can guide enterprises toward the most suitable financing path, ensuring a balance between immediate financial needs and long-term strategic goals.

Navigating the Loan Application Process for Conventional Commercial Loans: A Guide to Success

Securing a conventional commercial loan is pivotal for many businesses seeking financial growth or stability. The loan process can seem daunting, but understanding its intricacies can significantly enhance your chances of approval. This guide outlines the benefits of a well-prepared loan application, the necessary documentation, tips for success, and common pitfalls to avoid, aiming to demystify the process and set your business on the path to financial success.

The Benefits of Understanding the Loan Application Process

- Increased Efficiency: Knowing what documents and information are needed can streamline the application process, saving time and resources.

- Higher Approval Rates: A complete and well-prepared application improves approval chances by demonstrating professionalism and financial responsibility.

- Better Loan Terms: Demonstrating a solid financial position and understanding your business needs can lead to more favorable loan terms, including lower interest rates and more suitable repayment schedules.

Essential Documentation

The documentation required for a conventional commercial loan application often includes:

- Business Financial Statements: Balance sheets, income statements, and cash flow statements for the last 2-3 years to demonstrate financial health.

- Tax Returns: Business and personal tax returns for the past few years to verify income and tax compliance.

- Business Plan: A detailed plan outlining your business model, market analysis, management team, and financial projections.

- Credit Report: Both personal and business credit reports are used to assess creditworthiness.

- Collateral Documentation: Information on assets that will be used as collateral for the loan.

Tips for a Successful Application

- Prepare Thoroughly: Ensure all documents are accurate, up-to-date, and complete.

- Understand Your Financials: Be ready to explain your financial statements and projections, demonstrating your business’s viability and growth potential.

- Know Your Credit Score: Understand your credit position and any factors that may impact your loan application. Take steps to improve your credit score before applying.

- Be Clear About Your Needs: Clearly articulate how the loan will be used and how it fits into your overall business strategy.

- Choose the Right Lender: Research lenders to find one that best matches your business needs and has experience in your industry.

Common Pitfalls to Avoid

- Lack of Preparation: Only complete applications or documentation can lead to immediate rejection.

- Poor Financial Health: High levels of existing debt, low cash flow, or poor credit history can be red flags for lenders.

- Overextending: Asking for more money than you can realistically repay can jeopardize your loan application.

- Not Understanding Terms: Failure to understand the loan terms, including interest rates and repayment schedules, can lead to financial difficulties later.

Applying for a conventional commercial loan requires meticulous preparation and an understanding of what lenders seek. By carefully preparing your application and avoiding common pitfalls, you can increase your chances of securing a loan and obtaining favorable terms that support your business’s growth and financial health. Remember, a successful loan application is not just about getting access to funds; it’s about demonstrating your business’s viability, financial responsibility, and long-term potential. With the right approach, the loan application process can be a stepping stone to achieving your business objectives.

Navigating Regulatory Considerations in Conventional Commercial Loans: Ensuring Compliance for Success

Understanding and adhering to regulatory considerations is crucial when businesses secure conventional commercial loans. These regulations protect the lender and borrower, ensuring fair practices and financial stability. These regulatory considerations can be particularly stringent for specific industries or types of businesses, reflecting those sectors’ higher risks or specificities. This article provides an overview of the benefits of regulatory considerations in the commercial lending landscape and highlights the importance of compliance for businesses seeking financing.

The Importance of Regulatory Considerations

Regulatory considerations in commercial lending involve complex laws, regulations, and guidelines governing financial transactions. These may include requirements set by banking authorities, financial regulatory bodies, and even international financial standards, depending on the scope and scale of the business operations. The aim is to ensure transparency, accountability, and fairness in the lending process, thereby protecting the interests of all parties involved.

Benefits of Compliance

- Risk Management: Adhering to regulatory considerations helps identify and mitigate financial risks, ensuring that the business remains solvent and capable of repaying the loan.

- Market Reputation: Compliance demonstrates a business’s commitment to lawful and ethical practices, enhancing its reputation in the market and with potential investors.

- Access to Better Rates: Lenders may view businesses that consistently meet regulatory requirements as lower-risk, potentially qualifying for loans with more favorable terms and interest rates.

- Avoidance of Legal Penalties: Non-compliance can lead to hefty fines, legal battles, and even the revocation of business licenses. Understanding and adhering to regulations keeps businesses out of legal trouble.

- Operational Efficiency: Regulatory compliance often encourages businesses to maintain accurate and thorough financial records, which can lead to improved management practices and operational efficiency.

Industry-Specific Considerations

Specific industries, such as healthcare, finance, and real estate, face additional regulatory scrutiny due to the nature of their operations and the higher risks involved. For example, a real estate development company may need to comply with environmental regulations, zoning laws, building codes, and standard financial regulations. Understanding these industry-specific regulations is essential for businesses in these sectors to secure and manage their commercial loans successfully.

Steps to Ensure Compliance

- Stay Informed: Regularly update your knowledge of relevant laws and regulations, as these can change.

- Consult Experts: Engage legal and financial advisors specializing in your industry to navigate the complex regulatory landscape.

- Implement Compliance Programs: Develop and enforce internal policies and procedures to consistently meet regulatory requirements.

- Regular Audits: Conduct regular audits of your financial practices and loan management processes to promptly identify and rectify potential compliance issues.

Regulatory considerations play a critical role in the conventional commercial loan process, especially for businesses in highly regulated industries. Understanding and adhering to these regulations facilitates a smoother loan application process and offers numerous benefits, including risk mitigation, enhanced reputation, and operational efficiencies. By prioritizing compliance, businesses can secure the financing they need while maintaining a solid footing in their respective industries.

Mastering Loan Repayment: Strategies for Success with Conventional Commercial Loans

Navigating the repayment of conventional commercial loans is as crucial as securing the loan itself. Effective loan repayment management ensures financial stability and can save your business significant interest over time. This article offers insights into managing loan repayments, with strategies aimed at minimizing interest payments, exploring options for early repayment, and handling financial difficulties that might impact your ability to repay the loan.

Minimizing Interest Payments

Interest on loans can accumulate quickly, increasing the total amount you’ll need to repay. Here are strategies to minimize these payments:

- Opt for Shorter Loan Terms: While longer terms lower monthly payments, they also accrue more interest over time. If your cash flow allows, opting for a shorter repayment term can save on interest.

- Make Extra Payments: Additional payments toward the loan principal can significantly reduce the interest amount, as a lower principal balance means less interest accumulation.

- Refinance at Lower Rates: If interest rates have dropped or your business’s financial health has improved, refinancing the loan at a lower interest rate can reduce your interest burden.

Options for Early Repayment

Paying off your loan early can be a smart financial move, but it’s essential to understand the terms of your loan:

- Check for Prepayment Penalties: Some loans include penalties for early repayment, which could negate the benefits of paying off the loan sooner. Review your loan agreement to understand any penalties involved.

- Lump-sum Payments: If you come into extra funds, a lump-sum payment can significantly reduce your principal balance and, subsequently, the interest.

- Regular Extra Payments: Consistently making extra payments, even in small amounts, can shorten the loan term and decrease the total interest paid.

Handling Financial Difficulties

Unexpected financial challenges can arise, affecting your ability to meet loan obligations. Here’s how to handle such situations:

- Communicate with Your Lender: If you anticipate difficulty making payments, contact your lender early. Many are willing to work with borrowers to adjust repayment terms temporarily.

- Consider Loan Modification: Some lenders may agree to modify the terms of your loan, such as extending the repayment period or temporarily reducing the interest rate.

- Restructure Your Finances: Find ways to reduce expenses and improve cash flow. It might include renegotiating terms with vendors, increasing revenue streams, or prioritizing payments.

Effectively managing your loan repayments requires a proactive approach, from strategizing to minimize interest payments to being prepared to handle financial hiccups along the way. By employing these strategies, you can maintain control over your financial obligations, reduce the cost of borrowing, and position your business for long-term economic health. Remember, the goal is not just to repay your loan but to do so in a way most advantageous for your business’s financial future.

Securing Success: The Benefits of Risk Management When Taking on Debt

In the dynamic world of business finance, taking on debt through conventional commercial loans is a common strategy for growth and expansion. However, this approach comes with its set of risks. Effective risk management is crucial to safeguard a business’s financial health and ensure that the loan serves its intended purpose and contributes positively to its overall strategy. This article provides an overview of managing the risks associated with taking on debt, offering strategies to protect your business, and maximizing the benefits of your loan.

Understanding the Risks

Before diving into risk management strategies, it’s essential to understand the potential risks of taking on debt, which include:

- Cash Flow Pressure: Regular loan repayments can strain your business’s cash flow, especially if revenues are inconsistent.

- Interest Rate Fluctuations: Payment amounts for loans with variable interest rates can increase, affecting your budgeting and financial planning.

- Overleveraging: Too much debt can jeopardize your business’s financial stability, making it difficult to secure additional financing when needed.

Benefits of Effective Risk Management

Implementing robust risk management strategies when taking on debt can offer several benefits:

- Financial Stability: By ensuring that loan repayments are manageable within your business’s cash flow, you can maintain economic stability and avoid default.

- Improved Creditworthiness: Managing debt effectively can enhance your business’s credit rating, facilitating better terms on future financing.

- Strategic Growth: With prudent debt management, loans can be used strategically to fuel growth without compromising financial health.

Risk Management Strategies

- Thorough Planning: Before taking on debt, develop a detailed plan for how the funds will be used and how the loan will contribute to generating revenue. It helps ensure that the loan serves its intended purpose effectively.

- Cash Flow Management: Monitor your business’s cash flow closely. Implement measures, such as maintaining a reserve fund or adjusting operational budgets, to ensure that there is always sufficient cash on hand to meet loan obligations.

- Fixed vs. Variable Interest Rates: Consider the trade-offs between fixed and variable interest rates. While variable rates may offer lower initial payments, they can fluctuate. Fixed rates provide predictability in repayments, which can be beneficial for budgeting.

- Debt-to-income Ratio: Monitor your debt-to-income ratio closely to avoid overleveraging. This ratio should reflect a balance that supports growth while ensuring the business can comfortably meet its debt obligations.

- Contingency Planning: Develop a contingency plan for financial downturns or unexpected expenses. It might include identifying areas for cost reduction, accessing an emergency credit line, or renegotiating loan terms if necessary.

- Regular Review and Adjustment: Review your debt management strategy to adjust for changes in your business environment, financial performance, or interest rates.

Conclusion

Managing the risks associated with taking on debt is essential for any business looking to leverage loans for growth and expansion. By understanding the potential risks and implementing effective risk management strategies, companies can safeguard their financial health, maintain stability, and ensure that taking on debt contributes positively to their long-term success. Remember, taking on debt should always be to enhance the business’s value and capabilities, not to compromise its financial future.

Blanket Loan Rates: Your Key to Smart Property Investment

Unlocking the Mystery of Blanket Loan Rates

Unlocking the Mystery of Blanket Loan Rates

If you’re considering investing in real estate or financing multiple properties, you’ve likely come across the term ‘blanket loan.’ But what does it mean, and more importantly, how do the rates for these loans work?

In this guide, we’ll demystify the concept of blanket loans, delve into the factors that influence their rates, and provide actionable insights to help you secure the best possible rates. This guide is designed to equip you with the knowledge you need to navigate the world of blanket loans confidently.

What are Blanket Loans?

Blanket loans, or blanket mortgages, allow borrowers to finance more than one piece of real estate property under a single loan. Instead of taking out individual loans for each property, you can consolidate them under one blanket loan.

This type of loan is prevalent among real estate investors and developers who own multiple properties. For instance, a real estate developer building a housing complex with multiple units might use a blanket loan to finance the project. Similarly, an investor owning several rental properties might use a blanket loan to streamline financing and reduce administrative overhead.

One of the critical features of a blanket loan is the release clause. It allows the borrower to sell off individual properties covered by the loan without paying off the entire loan balance. For example, if you have a blanket loan on three properties and sell one, you can use the proceeds to pay off the portion of the loan related to that property while the loan continues to cover the remaining properties.

However, while blanket loans can offer convenience and flexibility, they also come with risks. One of the most significant risks is the cross-collateralization aspect of blanket loans. If you default on the loan, the lender has the right to seize all properties covered by the loan, not just the one that might be causing financial strain.

Understanding the ins and outs of blanket loans, including their rates, is crucial for anyone considering this type of financing. It allows you to weigh the benefits against the potential risks, helping you make an informed decision that aligns with your financial goals.

Why Understanding Blanket Loan Rates Matters

Blanket loan rates are a crucial aspect to consider when opting for this type of financing. The rate you secure on your blanket loan can significantly impact your investment’s overall cost and financial health in the long term. Here’s why understanding these rates is so important:

- Cost of Borrowing: The rate of your blanket loan determines the interest you’ll pay over the life of the loan. A lower rate means you’ll pay less interest, reducing the total cost of borrowing. Conversely, a higher rate increases the interest paid, making your loan more expensive.

- Monthly Payments: Your loan rate also affects your monthly payments. A lower rate can result in more manageable monthly payments, while a higher rate can lead to larger monthly payments. Understanding this can help you budget effectively and comfortably repay the loan.

- Investment Profitability: If you’re an investor or developer, the rate on your blanket loan can impact the profitability of your real estate investments. A lower rate can increase your potential profits, while a higher rate can affect your returns.

- Loan Comparison: Understanding blanket loan rates can also help you compare loan options. A blanket loan with a specific rate is more cost-effective than taking out individual loans for each property or vice versa.

- Negotiation Power: Knowledge is power. Understanding how blanket loan rates work can give you the upper hand when negotiating with lenders. You’ll be able to ask the right questions and potentially secure a more favorable rate.

In the following sections, we’ll delve into the factors influencing blanket loan rates and provide tips on securing the best rates. Knowledge can help you make informed decisions and potentially save a significant amount of money over the life of your loan.

What to Expect in this Guide

This comprehensive guide is designed to provide you with a deep understanding of blanket loan rates and how they work. Here’s a brief overview of what you can expect in the following sections:

- Unraveling the Concept of a Blanket Loan: We’ll look deeper into the concept of a blanket loan, discussing its advantages and disadvantages and the situations where it can be most beneficial.

- Factors That Influence Blanket Loan Rates: We’ll explore the factors that can affect the rates of blanket loans, such as your credit score, the real estate market conditions, the lender’s policies, and the overall economy.

- Comparing Blanket Loan Rates to Other Loan Rates: We’ll compare blanket loan rates with other types of loan rates, such as mortgage rates, commercial loan rates, and personal loan rates. It will help you understand where blanket loans stand in the broader loan market.

- How to Secure the Best Blanket Loan Rates: We’ll provide practical tips and strategies to help you secure the best possible rates on your blanket loan. It includes advice on shopping, understanding loan terms, and using loan brokers.

- Case Study: We’ll present a real-world case study of a successful experience with a blanket loan. It will provide practical insights and lessons you can apply to your situation.

- Frequently Asked Questions about Blanket Loan Rates: We’ll address some of the most common questions and misconceptions about blanket loan rates, providing clear and expert answers.

By the end of this guide, you should have a solid understanding of blanket loan rates and feel confident in making informed decisions about this type of financing. Whether you’re a seasoned investor or just starting, this guide will provide valuable insights to help you navigate the world of blanket loans.

Unraveling the Concept of a Blanket Loan

As mentioned earlier, a blanket loan is a unique type allowing borrowers to finance multiple properties under a single loan agreement. This type of loan is prevalent among real estate investors and developers, but it’s also used by businesses that need to finance multiple locations or equipment. Let’s delve deeper into the concept of a blanket loan and its various aspects.

The Mechanics of a Blanket Loan

A blanket loan works by consolidating multiple properties under one mortgage. Instead of taking out individual mortgages for each property, a borrower can take out one blanket loan to cover all properties. It can simplify the management of multiple properties, as there’s only one loan to keep track of, one payment to make, and one lender to deal with.

Advantages of a Blanket Loan

There are several advantages to using a blanket loan:

- Simplicity: Managing multiple properties and their respective loans can be complex. A blanket loan simplifies this process by consolidating everything under one loan.

- Cost Savings: In many cases, the costs associated with a blanket loan (such as closing costs) can be lower than if you were to take out individual loans for each property.

- Flexibility: Blanket loans often come with a release clause, which allows you to sell off individual properties without paying off the entire loan. It can provide flexibility in managing your real estate portfolio.

Risks and Disadvantages of a Blanket Loan

While a blanket loan can offer several advantages, it’s also important to be aware of the potential risks and disadvantages:

- Cross-Collateralization: In a blanket loan, all properties serve as collateral for the loan. If you default on the loan, the lender could seize all properties, not just the one causing financial strain.

- Difficulty in Finding Lenders: Only some lenders offer blanket loans, so finding a lender who does might take time and effort.

- Potential for Higher Interest Rates: Depending on the lender and your creditworthiness, the interest rates on blanket loans can sometimes be higher than those on individual mortgages.

Understanding these aspects of a blanket loan can help you decide whether this type of financing is right for you. In the next section, we’ll explore the factors influencing blanket loan rates, a crucial part of this decision-making process.

Defining a Blanket Loan

A blanket loan, also known as a blanket mortgage, is a type of loan that allows a borrower to finance multiple properties under one loan agreement. It differs from traditional loans, where each property requires its loan.

The term “blanket” in blanket loan refers to the loan coverage over multiple properties, much like a blanket covers you from head to toe. This type of loan is most commonly used in real estate, particularly by investors and developers dealing with more than one property.

For example, if a real estate investor owns several rental properties, they could use a blanket loan to finance them under one loan rather than having a separate mortgage for each parcel. Similarly, a real estate developer building a housing complex with multiple units could use a blanket loan to finance the project.

One of the key features of a blanket loan is the inclusion of a release clause. This clause allows the borrower to sell off individual properties covered by the loan without having to pay off the entire loan balance. For instance, if a borrower has a blanket loan covering three properties and decides to sell one, they can pay off the portion of the loan on that property, and the blanket loan will continue to protect the remaining properties.

However, it’s important to note that blanket loans also come with certain risks. Because all properties under the loan are collateral, the lender has the right to seize all properties covered if a borrower defaults. This cross-collateralization aspect is one of the reasons why understanding blanket loan rates and terms is crucial before deciding to take on this type of financing.

When to Use a Blanket Loan

Blanket loans can be valuable in certain situations, particularly for real estate investors, developers, and businesses. Here are some scenarios where a blanket loan might be beneficial:

- Real Estate Investors: If you’re an investor with multiple rental properties, a blanket loan can simplify your financing by consolidating all your properties under one loan. It can make managing your portfolio easier, as you’ll only have one loan payment and one set of loan terms to track.

- Real Estate Developers: Developers working on projects with multiple units, such as a housing complex or a condominium building, can use a blanket loan to finance the entire project. It can streamline the financing process and save on closing costs compared to securing individual loans for each unit.

- Businesses with Multiple Locations: Businesses operating in multiple locations, such as retail chains or restaurants, can use a blanket loan to finance their areas. It can be more efficient and cost-effective than securing separate loans for each location.

- Investors Looking to Expand: A blanket loan can finance multiple properties if you want to expand your portfolio quickly. Growing your portfolio can be faster and more efficient than securing individual loans for each new property.

- Borrowers Seeking to Refinance: If you already own multiple properties with separate loans, you might use a blanket loan to consolidate these loans into one. It could lower your overall interest rate and monthly payment and simplify the management of your properties.

While blanket loans can offer convenience and potential cost savings, they also come with risks, such as losing all properties to foreclosure if you default. Therefore, it’s essential to carefully consider your financial situation, investment strategy, and risk tolerance before deciding to use a blanket loan.

Factors That Influence Blanket Loan Rates

Like any other type of loan, the rates on blanket loans are influenced by various factors. Understanding these factors helps you anticipate what rate you are offered and can assist you in securing the best possible rate for your situation. Here are some of the key factors that influence blanket loan rates:

Your Credit Score

Your credit score is one of the most significant factors lenders consider when determining your loan rate. A higher credit score indicates that you’re at a lower risk to the lender, which can result in a lower interest rate. On the other hand, a lower credit score can lead to a higher interest rate. “The importance of credit score monitoring”

The Real Estate Market

The conditions of the real estate market can also impact blanket loan rates. In a booming market, lenders offer lower rates due to the properties’ increased value and potential profitability. Conversely, lenders increase rates in a slower market to offset the potential risk of property value decline.

Lender Policies

Each lender has their policies and criteria for determining loan rates. Some lenders might specialize in blanket loans and offer competitive rates, while others might view these loans as higher risk and charge higher rates. It is why shopping around and comparing rates from different lenders is crucial.

The Economy

Broader economic conditions can also influence blanket loan rates. Factors such as the state of the economy, inflation rates, and monetary policy can impact interest rates on all types of loans, including blanket loans.

The Properties Themselves

The characteristics of the properties being financed can also impact the loan rate. Factors such as the location, condition, type of properties, and total number of properties funded can influence the rate.

Understanding these factors can help you anticipate and negotiate your blanket loan rate. In the next section, we’ll provide tips on securing the best possible rate for your blanket loan.

Comparing Blanket Loan Rates to Other Loan Rates

When considering a blanket loan, comparing its rates to other types of loans is helpful. It can give you a better understanding of the cost of a blanket loan relative to other financing options. Here’s how blanket loan rates typically compare to different loan rates:

Blanket Loan Rates vs. Mortgage Rates

Blanket loans and traditional mortgages are used to finance real estate but serve different purposes; thus, their rates can differ. Conventional mortgage rates are often lower than blanket loan rates because a single property secures them, presenting less risk to the lender. On the other hand, Blanket loans cover multiple properties, which can introduce more complexity and risk, leading to higher rates.

Blanket Loan Rates vs. Commercial Loan Rates

Commercial loans finance commercial properties, such as office buildings or retail spaces. The rates on commercial loans can be similar to or higher than blanket loan rates, depending on factors like the borrower’s creditworthiness, the profitability of the commercial property, and the overall risk of the loan.

Blanket Loan Rates vs. Personal Loan Rates